The CTV Boomer: Why the Advertisers Riding This Wave Will Look Like Geniuses in Five Years

There is a generation of advertisers being created right now. They are quiet about it. They are not posting about it on LinkedIn. They are not shouting in conference panels. They are sitting in a planning meeting with their CFO, looking at the same chart you're about to look at, and reallocating dollars.

I call them the CTV Boomers.

Not because they are old. Because they are early — the same way the original boomers were early to network television, the same way the first wave of search advertisers were early to Google, the same way the first DTC brands were early to Facebook. They are showing up to a market while it is still uncrowded, while CPMs still reward early entrants, while the audience is rapidly migrating but the competitive set hasn't caught up yet.

And in five years, they are going to look like geniuses.

This is a post about why.

The chart that should be on every CMO's desk right now

In December 2025, Nielsen reported that streaming captured 47.5% of all US television viewing. On Christmas Day, it hit a single-day record of 54%. Linear broadcast and cable, combined, dropped to 41.6%. The transition has happened. It is no longer a forecast. It is the present tense.

Now look at where the dollars are.

US Connected TV ad spend in 2025 was $33.35 billion (eMarketer). Total US ad spend across all channels was over $400 billion. CTV captures 47.5% of attention. It captures roughly 8% of spend.

That gap is the entire opportunity. It is not a marketing slogan. It is a structural inefficiency in capital allocation across the entire ad industry — and inefficiencies of this magnitude do not last forever. They close. The only question is whether you are positioned on the early side of that closing or the late side.

The advertisers showing up early are not paying premium prices for premium audiences. They are paying underpriced prices for premium audiences, because the demand curve hasn't caught up to the supply of attention yet. That is what being early to a media wave actually means in dollar terms.

Blue ocean vs. red ocean — and where most advertisers are right now

I'm a believer in W. Chan Kim and Renée Mauborgne's Blue Ocean Strategy. Their framework, published by INSEAD in 2005 and now taught in nearly 3,000 universities, divides every market into two states.

Red oceans are the markets you already know. The boundaries are defined. The competitors are entrenched. Everyone is fighting for the same shrinking pool of attention with the same tactics, and the only way to win share is to outbid the next agency for the same impression. Margins compress. CPMs inflate. The water turns red because it is the blood of competitors fighting over a shrinking pie.

Blue oceans are the uncontested spaces. New demand. New rules. New audiences who have not yet been bid up to inefficiency. The competition is not absent — it just hasn't arrived yet. The value-cost trade-off that defines red oceans (you can have differentiation OR low cost, not both) breaks down. You can deliver more value at a lower cost simultaneously, because the market has not been arbitraged.

Look at where the average DTC brand is spending in 2026.

Meta. CPMs up roughly 20–30% year-over-year through 2024. The platform has saturated. Every category has hundreds of competitors bidding against you for the same household. Your creative refresh velocity has tripled in three years and your blended ROAS has barely moved.

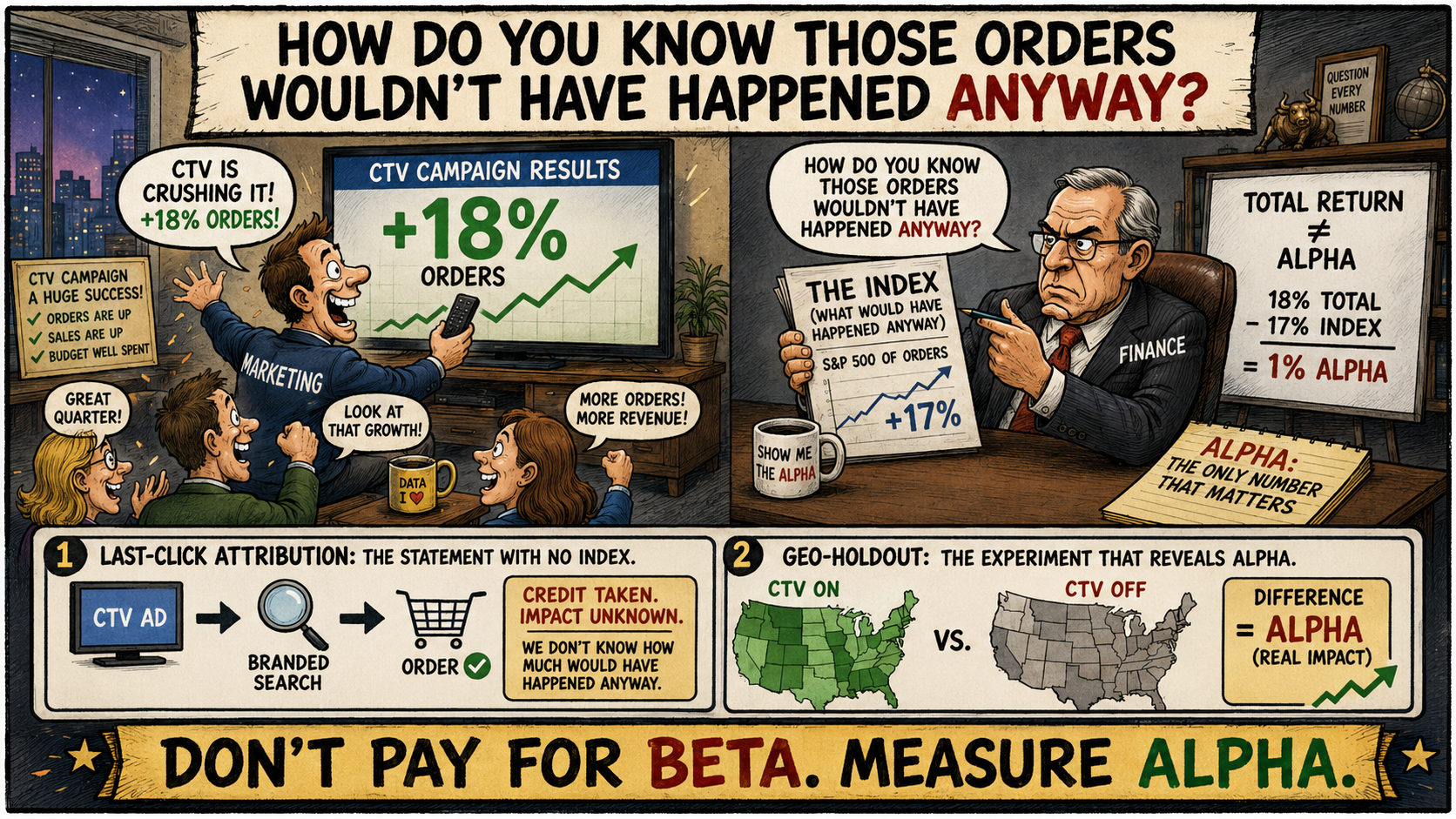

Google paid search. Branded keywords cannibalize organic demand you would have captured anyway. The Stella 2025 incrementality benchmark — 225 independent causal tests — found that Google branded search produced a median iROAS of 0.70x. That is the worst-performing channel in the modern paid stack, and most advertisers are still spending heavily on it because the dashboard reports look fine.

These are red oceans. The water has been red for years. Every additional dollar buys diminishing returns and you can feel it in the numbers, even if your team isn't saying so out loud.

CTV, right now, is blue water.

Why CTV is structurally a blue ocean (and how long it will stay one)

Three forces keep CTV in blue-ocean territory today, and one slowly closing window will eventually close it.

Force one: the audience migrated faster than the spend. Consumers cut the cord on a five-year accelerated curve. Disney went from no ad-supported tier to 164 million ad-supported MAU. Netflix went from "we'll never run ads" to 94 million ad-tier subscribers in two years. Antenna tracked 51.4 million billed ad-tier subscribers added in 24 months between Q1 2023 and Q1 2025. The audience is there. The advertisers are still catching up.

Force two: most agencies don't know how to buy CTV well. It is harder than search. It is harder than social. It requires premium supply path expertise, server-side conversion architecture, identity-graph integration, and incrementality validation that most generalist agencies haven't built. Brands that try to buy CTV through a generalist shop usually have a bad first experience, conclude "CTV doesn't work," and retreat to Meta. That misdiagnosis — we tried it and it didn't work — is currently subsidizing the brands that are doing it right.

Force three: the loudest critics on LinkedIn are scaring half the market away from the channel entirely. Every advertiser who reads a LinkedIn post and decides CTV is a scam is one more competitor not bidding against you tomorrow. Their absence is your discount. I will not name names. I will simply note that the most expensive consultancy in the world is the kind that costs you the next decade of growth because you listened.

The closing window: these forces are temporary. eMarketer projects US CTV ad spend to grow from $33.35B in 2025 to $46.89B by 2028, the year CTV surpasses traditional TV ad spend for the first time. As the dollars catch up to the eyeballs, CPMs will normalize, supply will get bid up, and the inefficiency will compress. The first-mover advantage closes around 2027–2028. After that, CTV is still a great channel — it is just no longer an unfair advantage.

The advertisers buying CTV right now are paying 2025 CPMs against 2027 audiences. That is what every previous media boom looked like. The first DTC brands on Facebook in 2013 paid $4 CPMs and built nine-figure businesses. By 2018 those CPMs had quadrupled. Same audience. Same channel. Different cost basis. The difference between the two cohorts wasn't strategy. It was timing.

What being a CTV Boomer actually looks like

I want to be specific here, because the difference between "spending in CTV" and "being a CTV Boomer" is the difference between buying a lottery ticket and compounding a portfolio.

A CTV Boomer buys premium supply, not open-exchange long-tail. They run on Disney, Netflix, Hulu, Peacock, Max, Paramount+, Tubi, the Roku Channel, and direct-sold inventory through trusted partners. They avoid the run-of-network programmatic that contains the documented IVT critics love to cite.

A CTV Boomer measures with server-side conversion APIs. They send conversion events directly from their backend CRM or point-of-sale to the ad platform, completely bypassing the user's browser. They recover the 30 to 40% of conversions that pixel-only tracking lost to iOS 14.5, Safari ITP, and ad blockers.

A CTV Boomer triangulates measurement. CAPI for daily tactical optimization. Bayesian Media Mix Modeling for strategic budget allocation. Geo-holdouts and incrementality testing for causal ground truth. The IAB has now standardized this approach in vendor-neutral guidance.

A CTV Boomer reads the primary sources. Not the LinkedIn hot takes. Not the dashboard. The Pixalate scope caveats. The IAS Media Quality Report. The IAB CAPI guidance. The MRC accreditation lists. The audited 8-K filings. They make decisions based on what the data actually says.

A CTV Boomer compounds. Most importantly, they do not view CTV as a quarterly experiment. They view it as a position. They build a base, they measure it, they expand it, and they let the compounding effect of brand-building plus performance lift run for 18 to 24 months. The advertisers that win on CTV are not the ones who tested it for six weeks and got nervous. They are the ones who committed to a multi-year build and watched their cost-per-acquisition curve descend while their competitors paid 30% more on Meta every year.

The historical pattern, briefly

I want to leave you with one historical pattern, because it is the pattern that has defined every media transition I have lived through in 25 years.

Network television in the 1950s. The first national advertisers — P&G, GE, Kraft — built brand equity that compounded for 50 years. The advertisers who waited for "proof" entered in the 1970s and paid 10x the CPM for a fraction of the differentiation.

Cable in the 1980s. Same pattern.

Search in the early 2000s. Brands that bid on Google at $0.05 CPCs in 2003 are still ranking organically in 2026 because of the data flywheel they built. Brands that waited until 2010 paid $5 CPCs for the same clicks and never caught up.

Facebook in 2013. The DTC brands that built audiences when CPMs were $4 — Warby Parker, Casper, Allbirds, Dollar Shave Club, Glossier — built nine and ten-figure businesses. The brands that arrived in 2018 paid four times as much for half the audience quality.

The pattern is not subtle. It repeats every time. And the people who tell you "wait until it's proven" are the same people who will, in 2030, write a LinkedIn post about how everyone should have been on CTV in 2026.

By then, CTV will be a red ocean. The premium inventory will be bid to efficiency. The CPMs will reflect demand. The competitive set will be saturated. And the CTV Boomers — the advertisers reading this in 2026 and acting on it — will have spent four years compounding an advantage their competitors will never close.

Closing

Cirque du Soleil did not become a $1B+ business by competing with Ringling Bros. They built a new market category — a blue ocean — and made the competition irrelevant.

Nintendo did not win the console wars by out-specing Sony. They built the Wii, then the Switch, in market segments their competitors had ignored. Blue ocean.

The advertisers who win the next decade of growth are not going to win it by paying 30% more on Meta than they paid last year. They are going to win it by being early to the channel where the audience already migrated, while their competitors were still arguing on LinkedIn about whether the channel was real.

Be a CTV Boomer.

Five years from now, you will be the one explaining to a junior marketer at a competitor company how you saw it coming when everyone else was looking the other way.

That story is still available to be written. The window is open. The data is on the table.

Sincerely,

Cory Poccia

CEO, CS & Co. Marketing Studio